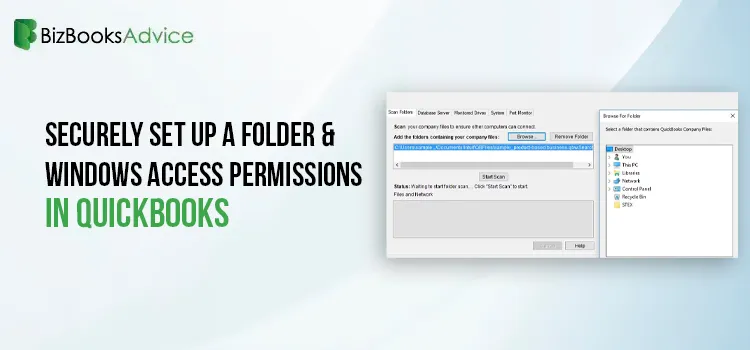

Securely Set up a folder & Windows access permissions in QuickBooks

Users require proper Windows user access permissions to run the folders in multi-use mode in QuickBo......

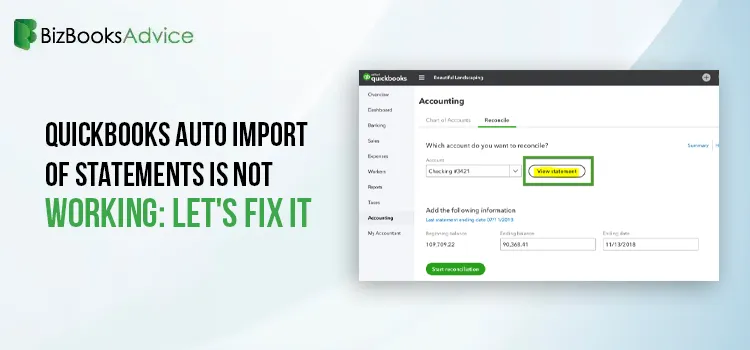

QuickBooks Auto Import of Statements is Not Working: Let’s Fix It

QuickBooks Auto-Import is a feature that allows you to automatically extract financial data. It may ......

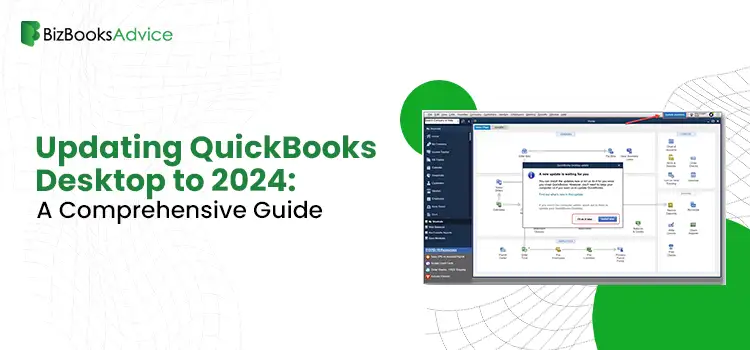

Update QuickBooks Desktop to 2024: Latest Features & Security Updates

Is your QuickBooks application working slowly or starting to freeze frequently? This issue may occur......

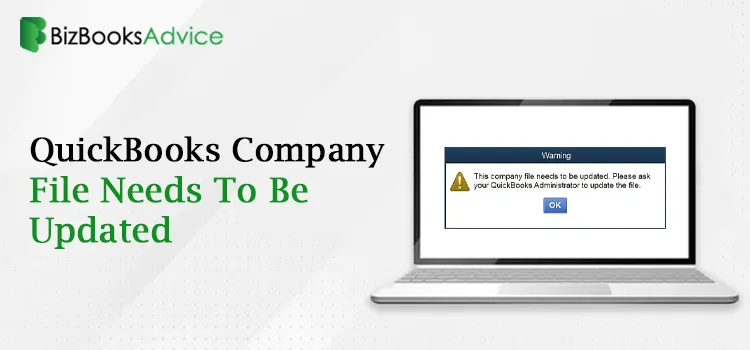

Why ‘This QuickBooks Company File Needs to Be Updated?’

Users get the QuickBooks Company file needs to be updated error message while attempting to launch a......

Fix QuickBooks Error H505 & Regain Access To Multi-User Mode

The QuickBooks Error H505 often appears with a warning message, “This company file is on another c......

How to Set Up QuickBooks Time Login & Fix Sign-In Issues?

Are you facing a QuickBooks Time login issue and unable to track the employees’ working hours?......

QuickBooks Update Stuck? Here’s How to Fix It Fast

Most often, the users may experience QuickBooks Update Stuck at 20-30% when it’s “Writing System......

Access QuickBooks GoPayment App: Take Payments On the Go

The QuickBooks GoPayment is a free mobile application for both Android and iOS users. Also, it allow......

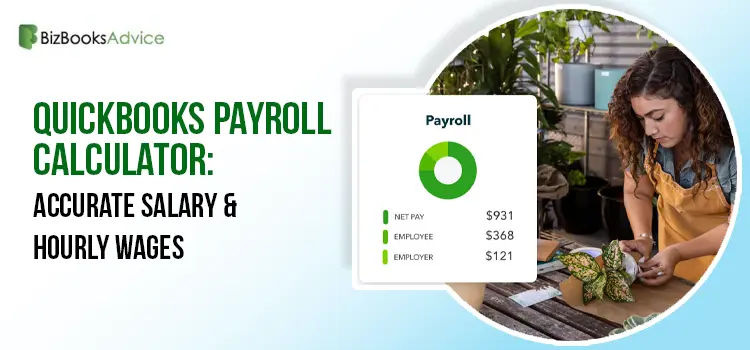

QuickBooks Payroll Calculator: Accurate Salary & Hourly Wages

Are you struggling while calculating your employees’ paychecks accurately? Well, in that case,......